ATCHAYA M

Developer

Updated on

04-03-2026

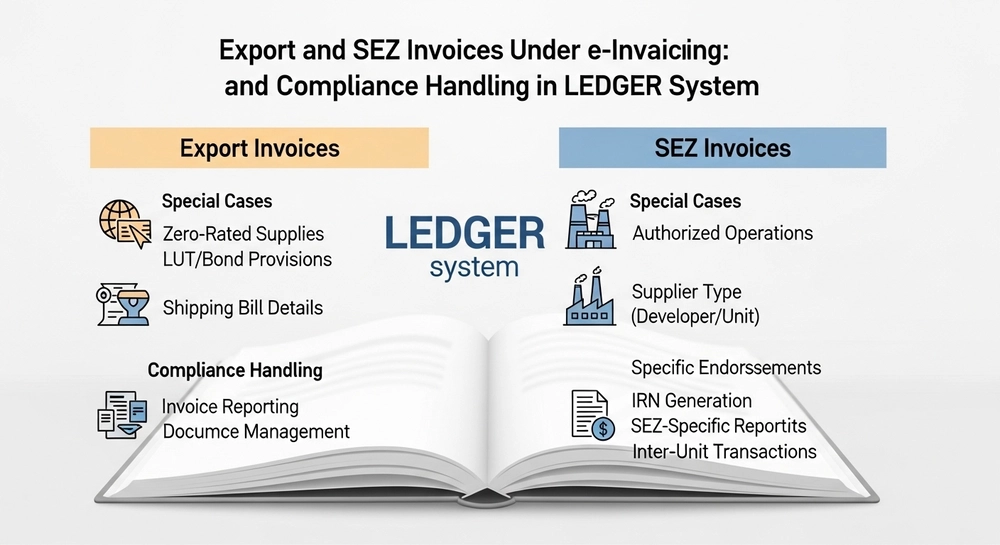

Export and SEZ Invoices Under e-Invoicing

Supplies made by exporters or suppliers to Special Economic Zones (SEZs) are treated as zero-rated for Goods and Services Tax (GST) purposes. In other words, these transactions do not have GST charged at the normal rate; however, they still must adhere to all reporting and documentation requirements. When you add e-invoicing to this mix, getting the data correct and ensuring clarity is even more critical.

Exporters and suppliers to SEZs often find that there are additional data fields, procedures and verification requirements associated with e-invoicing for exports and SEZs than for other types of domestic transactions. If an exporter or supplier fails to comply with the additional requirements or takes a casual approach to handling them, the exporter or supplier could experience delays in obtaining refunds for federal or state taxes, problems with reconciliation, or inquiries from the Internal Revenue Service (IRS). Therefore, having a basic understanding of how e-invoicing and zero-rated supplies affect exporters or suppliers to SEZs is crucial for businesses to avoid complications.

Understanding Zero-Rated Supplies in Exports and SEZ Transactions

Exporters and suppliers to SEZ units or developers are treated as zero-rated supplies under GST law. An exporter or supplier may choose to:

- Exporting under a letter of undertaking (LUT) will allow the exporter to avoid paying IGST

- Exporting with IGST and requesting a refund later.

Both of these export options require proper documentation and consistent reporting across e-invoicing, GST returns, and refund requests.

Although the procedures associated with exports follow common practices as described above, there are some unique procedures that must be followed to verify that authorized operations have occurred and that an endorsement of proper operation has been issued in regard to the supply of goods or services.

Why Export and SEZ Invoices Need Special Attention in e-Invoicing

Unlike regular B2B invoices, export and SEZ invoices contain additional information that must be captured correctly during IRN generation. These include:

- Shipping bill number and date

- Port code

- Country of destination

- Supply type (export with payment / without payment)

- SEZ registration details

If any of these fields are missing or incorrectly entered, the invoice may fail validation or create problems during return filing and refund processing.

Because of this, export and SEZ invoices require more careful preparation than standard domestic invoices.

Handling LUT and IGST Options Correctly

Businesses exporting without payment of tax must operate under a valid LUT. If the LUT is not active or details are missing, the invoice may be treated incorrectly during reporting.

On the other hand, when exporting with IGST payment, the tax must be properly reflected in the invoice and later reconciled with refund claims.

In practice, mistakes in selecting the correct option can result in:

- Incorrect tax reporting

- Delayed refunds

- Compliance notices

Maintaining clarity at the invoicing stage helps prevent these downstream issues.

Shipping and Logistics Details in e-Invoicing

Export transactions are closely linked with logistics and customs documentation. Shipping bills, airway bills, and port details become part of the compliance ecosystem.

When these details are not aligned between e-Invoices, shipping documents, and GST returns, authorities may raise questions during verification.

A well-prepared export invoice ensures that:

- Shipping data matches invoice records

- Customs documentation aligns with GST filings

- Refund applications are supported by consistent data

This reduces friction during cross-border trade compliance.

SEZ-Specific Documentation Requirements

Supplies to SEZ units are considered zero-rated only when they are meant for authorized operations. This usually requires proper endorsement and supporting documentation.

Under e-Invoicing, SEZ invoices must clearly indicate:

- SEZ unit or developer status

- Authorized operation reference

- Supply classification

Without these indicators, transactions may be treated as regular domestic supplies, affecting tax treatment and compliance reporting.

Return Filing and Refund Implications

Export and SEZ invoices directly affect:

- GSTR-1 reporting

- Refund claims under GST

- ITC utilization patterns

- Annual reconciliation

Errors in e-Invoiced export data often surface during refund processing, when authorities compare IRP data, GST returns, and shipping records.

Businesses that maintain consistency across these stages face fewer delays and fewer documentation requests.

Why a Structured e-Invoicing Approach Helps Exporters

Exporters and SEZ suppliers usually operate with tight timelines, currency fluctuations, and regulatory scrutiny. Managing compliance through scattered systems increases risk.

A structured e-Invoicing workflow helps businesses:

- Maintain clarity across international and domestic reporting

- Reduce refund processing delays

- Improve audit readiness

- Avoid repeated documentation follow-ups

It also strengthens credibility with banks, customs authorities, and trade partners.

Conclusion

Export and SEZ invoicing under e-Invoicing involves more than generating IRN numbers. It requires careful attention to tax treatment, shipping data, regulatory options, and return reporting. Small mistakes at the invoice stage can create significant delays later in refunds, reconciliations, and audits.

By understanding these special requirements and following disciplined documentation practices, businesses can manage export and SEZ compliance more efficiently. A consistent and well-connected invoicing process not only ensures regulatory compliance but also supports smoother international and SEZ operations in the long run.