VAIRAVAN K

Senior Developer

Updated on

13-05-2026

Coverage of Journal Entry Types in Accounting

Every transaction your business records starts as a journal entry. Whether you sell a product, pay a bill, or adjust your stock, that movement of money or value enters your books through a journal. Most business owners think of journal entries as a single concept, but accountants actually deal with several distinct types, each serving a specific purpose in the accounting cycle.

Understanding these types matters more than you might think. The wrong entry in the wrong place can throw off your financial statements, mislead your tax filings, and turn a clean audit into a long evening of reconciliation. So let us walk through the main journal entry types you will encounter, what they do, and when to use each one.

Why Journal Entries Matter

At its core, accounting is the language of business, and journal entries are its sentences. Every entry follows the double entry accounting principle, which means each transaction touches at least two accounts, one debit and one credit. The total debits must always equal the total credits, keeping your books mathematically sound.

When you record entries correctly, your trial balance reconciles smoothly, your profit and loss statement reflects reality, and your balance sheet tells the true story of your business. When you record them incorrectly, every report downstream carries that mistake forward.

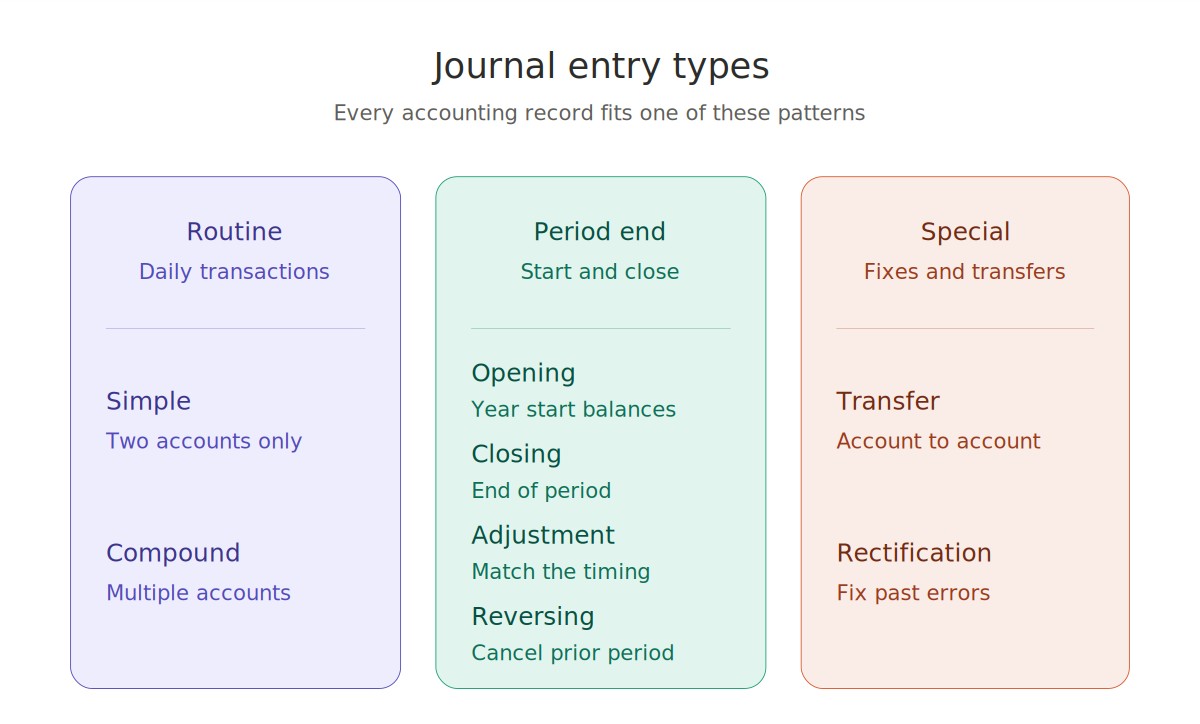

Simple Journal Entries

A simple journal entry involves just two accounts. One account receives a debit, and the other receives a credit. This is the most common type of entry you will record, and it usually covers everyday transactions.

For example, when your business pays the electricity bill in cash, you debit the Electricity Expense account and credit the Cash account. Two accounts, one transaction, clean and straightforward. Most retail sales, basic expense payments, and routine deposits fall into this category.

Compound Journal Entries

Sometimes a transaction touches more than two accounts. That is where compound journal entries come in. These entries debit one or more accounts and credit one or more accounts within a single record.

Say you buy office furniture for fifty thousand rupees, pay thirty thousand in cash, and put the rest on credit. The entry debits the Furniture account for the full fifty thousand, credits Cash for thirty thousand, and credits Accounts Payable for twenty thousand. One transaction, three accounts, all balanced.

Compound entries save time and keep related movements together, which makes them especially useful for payroll, asset purchases with mixed payments, and tax inclusive sales.

Opening Journal Entries

When you start a new financial year, the closing balances from the previous year carry over as opening balances for the new one. Opening journal entries record this transfer so your books begin the year with the correct numbers.

These entries cover assets, liabilities, and capital balances. They are usually posted on the first day of the financial year and form the foundation for every transaction that follows. If you migrate to a new accounting platform like Ledgers, opening entries also help you bring forward historical balances cleanly.

Closing Journal Entries

At the end of the financial year, you need to close out your temporary accounts. Revenue, expense, and drawing accounts get transferred to the capital or retained earnings account through closing entries.

The goal here is simple. Temporary accounts should reset to zero at the start of each new period, while permanent accounts on the balance sheet carry forward. Closing entries make this happen and prepare your books for the next year.

Adjustment Entries

Not every transaction is straightforward. Some require adjustment entries to align your books with the actual financial position at period end. These usually appear during month end or year end closing.

Common adjustment entries include accrued income, accrued expenses, prepaid expenses, depreciation, and unearned revenue. For instance, if you paid your annual insurance premium in April, you would adjust each month to recognize one twelfth of the premium as an expense, leaving the rest as a prepaid asset.

Adjustment entries follow the matching principle, which ensures expenses appear in the period they helped generate revenue.

Transfer Journal Entries

Transfer entries move balances between accounts without changing the total value. You might transfer funds from one bank account to another, shift profit to a reserve, or move a balance from a control account to a sub ledger.

These entries do not affect your overall financial position but help organize how money flows within your business. Inside Ledgers, transfer entries are particularly handy for managing multiple bank accounts and inter branch movements.

Rectification Entries

Mistakes happen. Wrong amounts, swapped debits and credits, postings to the wrong account, all of these need correction. Rectification entries fix errors discovered after the original entry has been posted.

The approach depends on when you spot the error. If you find it before the trial balance is prepared, a simple correction may suffice. If the error surfaces after preparing financial statements, you may need to pass a formal rectification entry that adjusts both the wrong and right accounts.

Reversing Entries

Reversing entries are made at the beginning of a new accounting period to cancel certain adjusting entries from the previous period. They are optional but useful, especially for accrued income and expenses.

By reversing the prior period adjustment, the new period entries become simpler, and you avoid double counting. Most accounting software, including Ledgers, can automate reversing entries so they post automatically on the first day of the next period.

Making Journal Entries Easier

Manually managing all these entry types across hundreds of transactions can become overwhelming. That is where a smart accounting platform helps. Ledgers automates routine entries, validates debit credit balances in real time, and applies the right entry type based on the transaction you record.

From GST invoices to payroll and reconciliation, Ledgers handles the heavy lifting so you can focus on running your business. Understanding the types of journal entries is essential, but using a system that gets them right the first time saves both time and worry.