VAIRAVAN K

Updated on

30-07-2026

Depreciation in Financial Statements: What It Means and Why It Matters

Every business owns things that wear out over time. A delivery truck doesn't last forever. A machine on the factory floor gradually loses its edge. Even the laptop your accountant uses every day is slowly becoming less valuable. Accounting has a way of capturing this reality, and it is called depreciation.

If you have ever looked at a set of financial statements and wondered why there is a line that seems to reduce the value of assets year after year, this article is for you.

What Is Depreciation?

Depreciation is the process of allocating the cost of a tangible asset over its useful life. Rather than recording the full cost of an asset as an expense when you buy it, you spread that cost across the years you expect to use it.

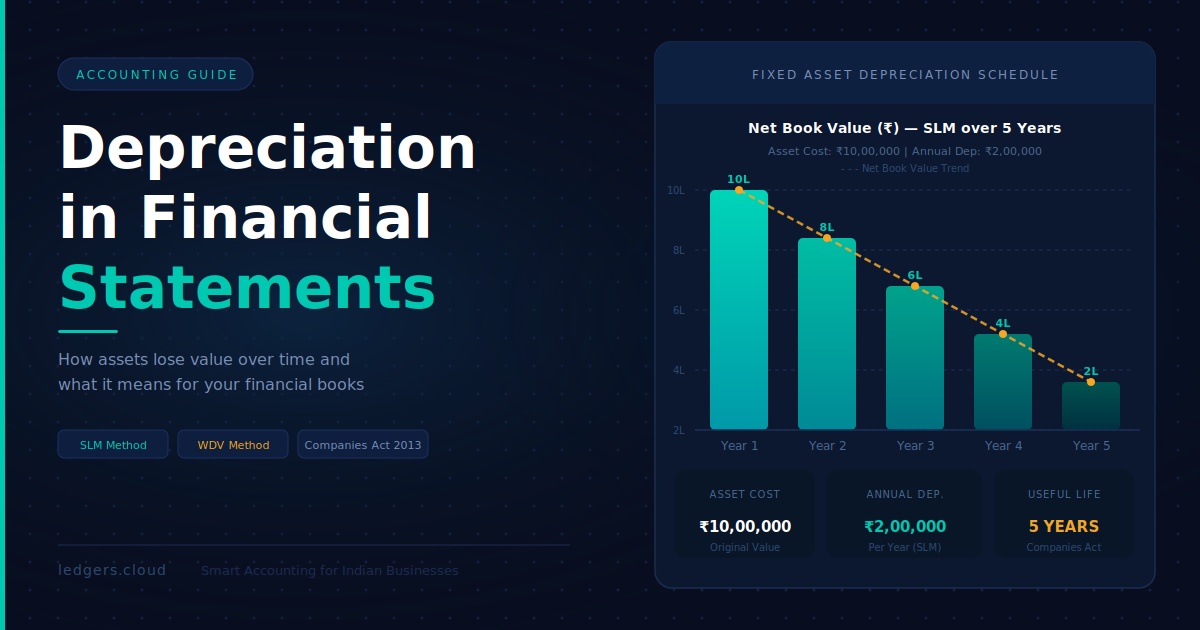

Think of it this way. If you purchase machinery worth ₹10,00,000 and expect to use it for 10 years, it would be misleading to show a ₹10 lakh expense in year one and nothing in the following nine years. Depreciation smooths this out, charging ₹1 lakh every year to reflect the ongoing economic use of that asset.

This approach follows the matching principle in accounting, which says expenses should be recognised in the same period as the revenue they help generate.

Where Depreciation Appears in Financial Statements

Depreciation does not live in just one place in your financial statements. It shows up in at least two of the three core reports, and understanding where it appears is key to reading your books correctly.

On the Income Statement, depreciation appears as an operating expense. It reduces your profit before tax, which means it also reduces your tax liability. This is one reason depreciation matters from a planning perspective, not just an accounting one.

On the Balance Sheet, depreciation accumulates over time as a figure called accumulated depreciation. This is shown as a deduction against the gross value of your fixed assets, giving you the net book value of those assets. For example, if a piece of equipment originally cost ₹5,00,000 and has accumulated depreciation of ₹2,00,000 over two years, the balance sheet will show it at a net book value of ₹3,00,000.

On the Cash Flow Statement, depreciation is added back under operating activities. This might seem counterintuitive at first. The reason is that depreciation is a non-cash expense. It reduces profit, but no cash actually leaves your bank account when you record it. So when preparing the indirect cash flow statement, you start with net profit and add depreciation back to arrive at the actual cash generated from operations.

Common Methods of Depreciation

Businesses in India can choose from several depreciation methods, and the choice affects how expenses are distributed across years.

Straight-Line Method (SLM) is the simplest. You divide the asset's depreciable cost equally across its useful life. It is predictable and easy to explain to stakeholders. The Companies Act 2013 prescribes useful lives for various asset categories, which businesses must follow when preparing statutory accounts.

Written Down Value Method (WDV) charges depreciation on the reducing balance of an asset each year. This means higher depreciation in early years and lower amounts as the asset ages. The Income Tax Act generally requires WDV for calculating depreciation for tax purposes, which is why you often see two different depreciation figures in a company's books.

Units of Production Method ties depreciation to how much an asset is actually used. If a machine produces 1,000 units this year out of a lifetime capacity of 10,000 units, it depreciates by 10% of its depreciable cost. This method makes sense for assets whose wear is directly tied to production volume.

Why Depreciation Matters to Business Owners

Depreciation is not just a number your accountant worries about. It has real implications for your business decisions.

First, it affects your reported profit. A business with significant capital assets will show lower profits because of depreciation charges, even if cash flow is strong. Understanding this distinction helps you evaluate performance more accurately.

Second, it influences your tax liability. Under the Income Tax Act, depreciation reduces your taxable income. Choosing the right method and asset classification can have a meaningful impact on your tax outgo each year.

Third, it informs your asset replacement strategy. Tracking net book values and accumulated depreciation gives you a clear picture of when assets are nearing the end of their useful life and when you might need to budget for replacements.

Finally, it affects key financial ratios. Return on assets, asset turnover, and EBITDA all interact with how depreciation is handled. Lenders and investors pay close attention to these numbers.

A Common Mistake to Avoid

Many small business owners treat depreciation as a purely mechanical exercise and delegate it entirely without understanding it. This can lead to errors in asset classification, wrong useful life assumptions, or missed adjustments when assets are sold or scrapped.

If your business manages fixed assets across multiple categories, getting the depreciation right from the start is much easier than correcting it later during audits or tax assessments.

Tools like Ledgers simplify this by automating asset tracking, depreciation calculations, and financial statement generation, so you always have accurate, audit-ready accounts without spending hours on spreadsheets.

The Bottom Line

Depreciation is one of those accounting concepts that can feel abstract until you see it reflected in your own financial statements. At its core, it is about honesty: presenting an accurate picture of what your assets are truly worth and what it actually costs to run your business over time.

Once you understand where it appears and why, your financial statements become much easier to read and much more useful for making decisions.