VAIRAVAN K

Updated on

30-07-2026

Merchant Exports and GST Invoicing in India: A Complete Guide

If you are a business that sources goods from manufacturers and sells them to buyers abroad, you are what the GST law calls a merchant exporter. It sounds simple enough, but the compliance side of things, especially around invoicing and tax, can get surprisingly layered. This guide breaks it all down in a way that actually makes sense.

What Is a Merchant Exporter Under GST?

A merchant exporter is any person or entity registered under GST who purchases goods from a supplier and exports them without processing or manufacturing anything themselves. Unlike a manufacturer exporter, a merchant exporter does not add any transformation to the product. They are essentially a trade intermediary in the export chain.

This distinction matters a lot under GST because the rules around procurement, invoicing, and refunds work differently for merchant exporters compared to manufacturer exporters.

How GST Applies to Merchant Exports

Exports in India are classified as zero-rated supplies under Section 16 of the IGST Act. This means the final export transaction itself carries a 0% tax rate. But here is the catch: the merchant exporter still buys goods from domestic suppliers, and those purchases attract GST.

So what happens to that input tax? There are two ways to handle it:

Option 1: Export Under LUT Without Paying IGST

The most common route is to file a Letter of Undertaking (LUT) with the GST department before the start of the financial year. Once the LUT is in place, the merchant exporter can export goods without paying IGST on the export invoice. They can then claim a refund of the unutilized Input Tax Credit (ITC) accumulated from purchases.

Option 2: Pay IGST and Claim Refund

Alternatively, the merchant exporter can pay IGST on the export invoice and claim a refund afterward. This route involves more upfront cash outgo, so most exporters prefer the LUT path.

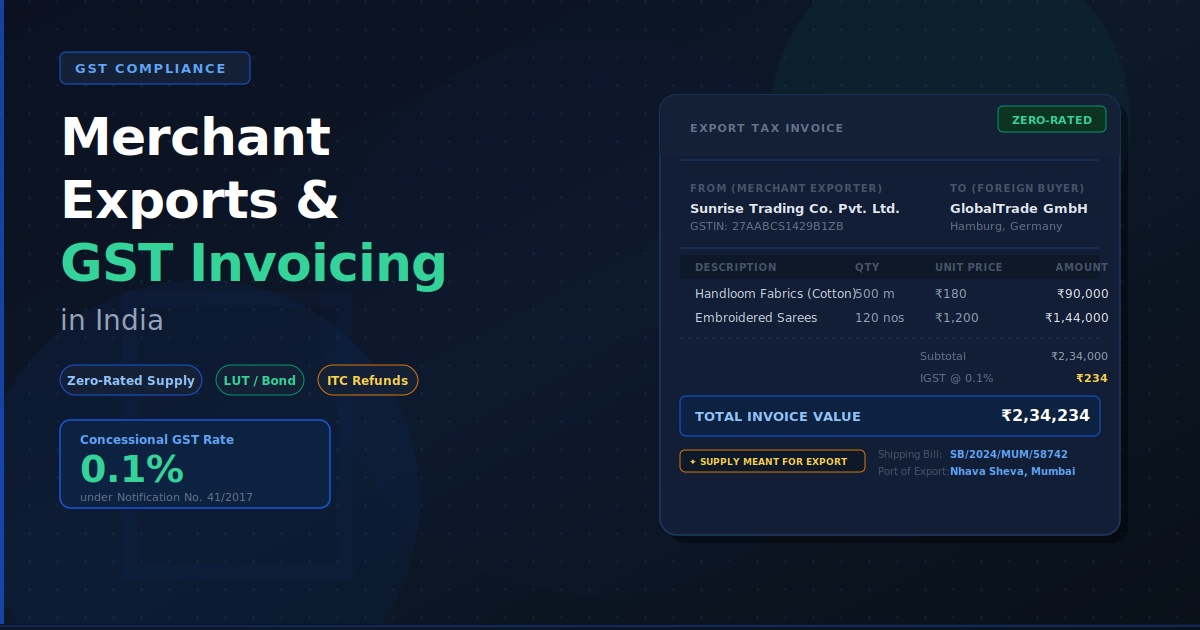

The 0.1% Concessional GST Rate for Merchant Exporters

One of the most useful provisions for merchant exporters is Notification No. 41/2017 (Integrated Tax Rate). Under this notification, a merchant exporter can procure goods from a registered supplier at a concessional GST rate of just 0.1% (instead of the standard rate) if certain conditions are met:

- The merchant exporter must be registered under GST

- The goods must be exported within 90 days from the date of the supplier's tax invoice

- The export must be made under a Letter of Undertaking or bond

- The merchant exporter must indicate on the supplier's invoice that the supply is meant for export

- The shipping bill or bill of export number must be provided to the supplier within 30 days of the export being made

If any of these conditions are not met, the supplier becomes liable to pay the full GST that was originally forgone. So the merchant exporter needs to be organized and timely.

GST Invoicing Requirements for Merchant Exports

Getting the invoice right is non-negotiable. Whether you are raising an invoice for a domestic procurement or an export transaction, each document must carry specific details.

For the Procurement Invoice (from Supplier to Merchant Exporter)

When a supplier invoices a merchant exporter under the 0.1% scheme, the document must clearly mention the merchant exporter's name and GSTIN, a declaration that the supply is meant for export, and the GST charged at the concessional rate.

For the Export Invoice (from Merchant Exporter to Foreign Buyer)

The export invoice raised by the merchant exporter must include:

- Supplier's name, address, and GSTIN

- Invoice number and date

- Description, quantity, and value of goods

- The phrase "SUPPLY MEANT FOR EXPORT UNDER LETTER OF UNDERTAKING WITHOUT PAYMENT OF IGST" or "SUPPLY MEANT FOR EXPORT ON PAYMENT OF IGST" as applicable

- The shipping bill number and port of export (once available)

Many businesses use Ledgers to generate export-compliant GST invoices that include all the mandatory fields, reducing the risk of errors that could delay refund claims.

Reporting Merchant Exports in GSTR-1

Merchant exporters need to report their export invoices in GSTR-1 under the relevant export tables:

- Table 6A is used for export invoices with or without payment of IGST

- Table 9 captures any amendments to previously reported export invoices

It is important that the details entered in GSTR-1 match exactly with what has been filed in the shipping bill on the ICEGATE portal. Any mismatch between these two systems can result in refund delays or rejections.

Refund Claims: What Merchant Exporters Need to Know

If you exported under LUT, you can claim a refund of unutilized ITC by filing Form RFD-01 on the GST portal. The refundable amount is calculated using a CBIC formula, and not all accumulated ITC gets refunded in a single cycle.

Refund claims must be filed within two years from the date the Export General Manifest (EGM) is filed. Keeping your books updated through a tool like Ledgers makes this process significantly less stressful when refund season arrives.

Common Mistakes to Avoid

- Missing the 90-day export window after the concessional procurement invoice date

- Not providing the shipping bill number to the supplier within the stipulated time

- Mismatch between GSTR-1 export data and ICEGATE shipping bill details

- Failing to mention LUT details on the export invoice

Final Thoughts

Merchant exports sit at the intersection of domestic GST compliance and international trade regulations, which makes them a bit more demanding than regular B2B or B2C transactions. But with the right invoicing process and timely filing habits, you can make the most of the zero-rated export benefit and recover your input taxes without much friction.

If you are a merchant exporter looking to streamline your GST invoicing and refund tracking, Ledgers is built exactly for that. From generating export invoices to managing GSTR-1 filings, the platform keeps you compliant and audit-ready at every step.