PUGALENTHI

Updated on

12-01-2026

Eligible vs Ineligible ITC: Practical Examples

In terms of reporting under the GST system, knowledge of how input taxes will affect their total tax liability helps the business remain compliant and optimize tax. Essentially, this guide – Eligible and Ineligible Inputs Tax Credit – Practical Examples provides insight into the eligible and ineligible Input Tax Credit (ITC) available under GST, by providing relatable examples of business scenarios. These examples help to provide clarity to the user as well as emphasizing the effect compliance may have on the ITC claims made by the user.

Understanding Input Tax Credit (ITC)

Input Tax Credit (ITC) is a mechanism that allows businesses to reduce the tax they have paid on inputs (raw materials, goods, services used in production) from their output tax liabilities. Essentially, ITC helps avoid the cascading effect of taxes, facilitating smoother financial operations for businesses. However, not all taxes paid can be claimed as ITC; distinguishing between eligible and ineligible ITC is vital for GST compliance.

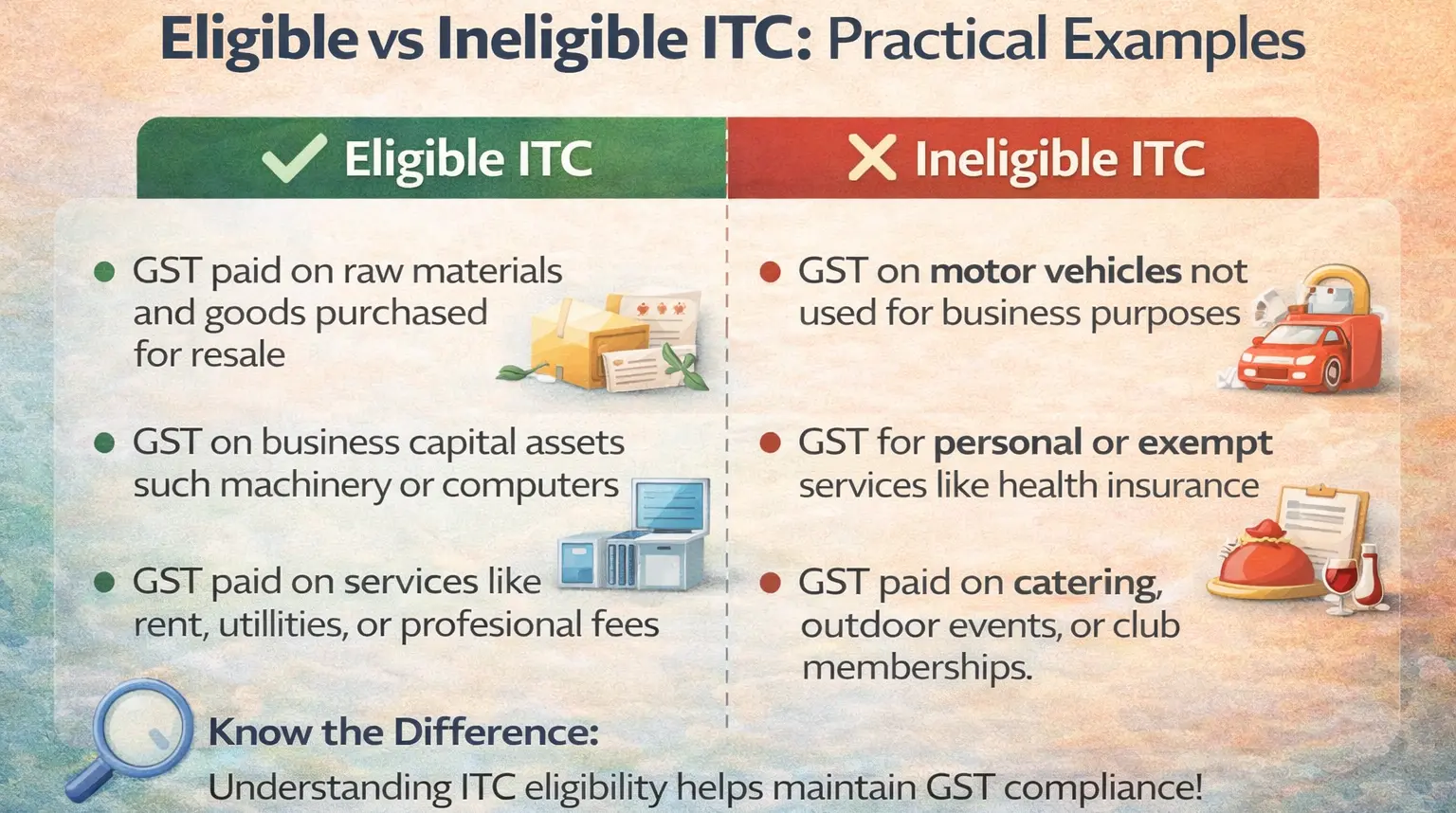

Eligible ITC: Common Examples

Eligible ITC refers to the GST paid on inputs that can be claimed against the output tax. Here's what usually qualifies as eligible ITC:

- Goods or Services Used for Business: All goods or services purchased for business purposes are generally eligible for ITC.

- Telecommunication Services: Costs associated with business communication systems are claimable.

- Stationery and Office Equipment: Items used in the daily functioning of office operations are eligible.

- Transportation Services: Transport used for moving goods for business transactions qualifies for ITC.

For instance, if a printing business purchases machinery or paper, the GST paid on these products can be claimed as ITC since they directly relate to the production process.

Ineligible ITC: Restricted and Blocked Credits

Certain situations restrict businesses from claiming ITC, termed as ineligible ITC. Understanding these restrictions can prevent compliance issues and unnecessary penalties:

- Motor Vehicles: ITC on motor vehicles is blocked unless the business itself is in the vehicle supply business or a handful of other specified services.

- Personal Use: Goods or services used for personal consumption are not eligible for ITC.

- Construction Services: Any GST paid for construction activities is not claimable unless the business involves such work.

- Membership to Clubs: Fees for club memberships or healthcare for employees are ineligible for ITC.

- Works Contract: GST paid on works contracts services if used for construction (excluding plant and machinery) is not claimable, except under specified conditions.

An example is seen in a corporate office refurbishing its spaces. While the office equipment purchase may be eligible, the cost of interior decoration services will not be claimable as ITC due to its categorization as a works contract service.

Why Certain Credits Cannot be Claimed

Understanding why certain credits are restricted is key to navigating GST provisions effectively:

- Preventing Misuse: Restrictions on personal use goods prevent businesses from lowering tax liabilities unfairly.

- Encouraging Compliance: By disallowing certain claims, businesses are nudged towards maintaining compliance and transparency.

- Revenue Safeguards: Some restrictions help prevent loss of revenue that may occur through excessive claims.

Compliance Impact and Practical Understanding for Businesses

The distinction between eligible and ineligible ITC has direct implications on compliance:

- Accurate Record-Keeping: Businesses must maintain meticulous records to justify claims.

- Regular Updates: Staying informed on GST amendments is crucial to avoid inadvertent errors.

- Professional Consultation: Engaging with GST experts can help navigate complex scenarios and ensure compliance.

For instance, a retail chain might find it beneficial to consult a GST professional to decide which promotional activities' expenses are ITC eligible, ensuring they don't miss out on legitimate claims.

Conclusion

To sum up, it is critical that businesses operating under GST have a thorough practical understanding of Eligible versus Ineligible ITC: Practical Examples. Distinguishing between input tax credits that are eligible and input tax credits that are not eligible will enable businesses to optimize their tax liability as well as facilitate a business's compliance with GST laws/regulations. Knowing what types of input tax credits can be classified as eligible and ineligible will also help prevent any errors businesses may make, and promote a systematic method to managing taxes. Overall, the purpose of this guide is to educate businesses about Eligible versus Ineligible Input Tax Credit and give them the practical information needed for the effective use of ITC consistent with GST regulatory requirements.

In a constantly evolving tax landscape, staying abreast with the latest GST updates and their impact on ITC eligibility remains a strategic priority for businesses aiming to thrive financially.

LEDGERS simplifies GST compliance by embedding reconciliation directly into the accounting workflow, helping businesses identify mismatches early and address them before they lead to interest or penalties. With automated GSTN data synchronization, invoice-level tracking, and system-driven validations, LEDGERS enables seamless, reliable compliance without last-minute corrections or manual follow-ups.