VAIRAVAN K

Senior Developer

Updated on

20-05-2026

GSTR-1 Explained: What Every Indian Business Owner Needs to Know

If you run a business in India and are registered under GST, GSTR-1 is a return you simply cannot ignore. It sounds technical, and the first time you encounter it, it probably feels that way too. But once you understand what it actually asks for and why it exists, filing it becomes far less intimidating. This guide breaks it all down in plain terms so you can stop dreading the due date and start managing it with confidence.

What Is GSTR-1?

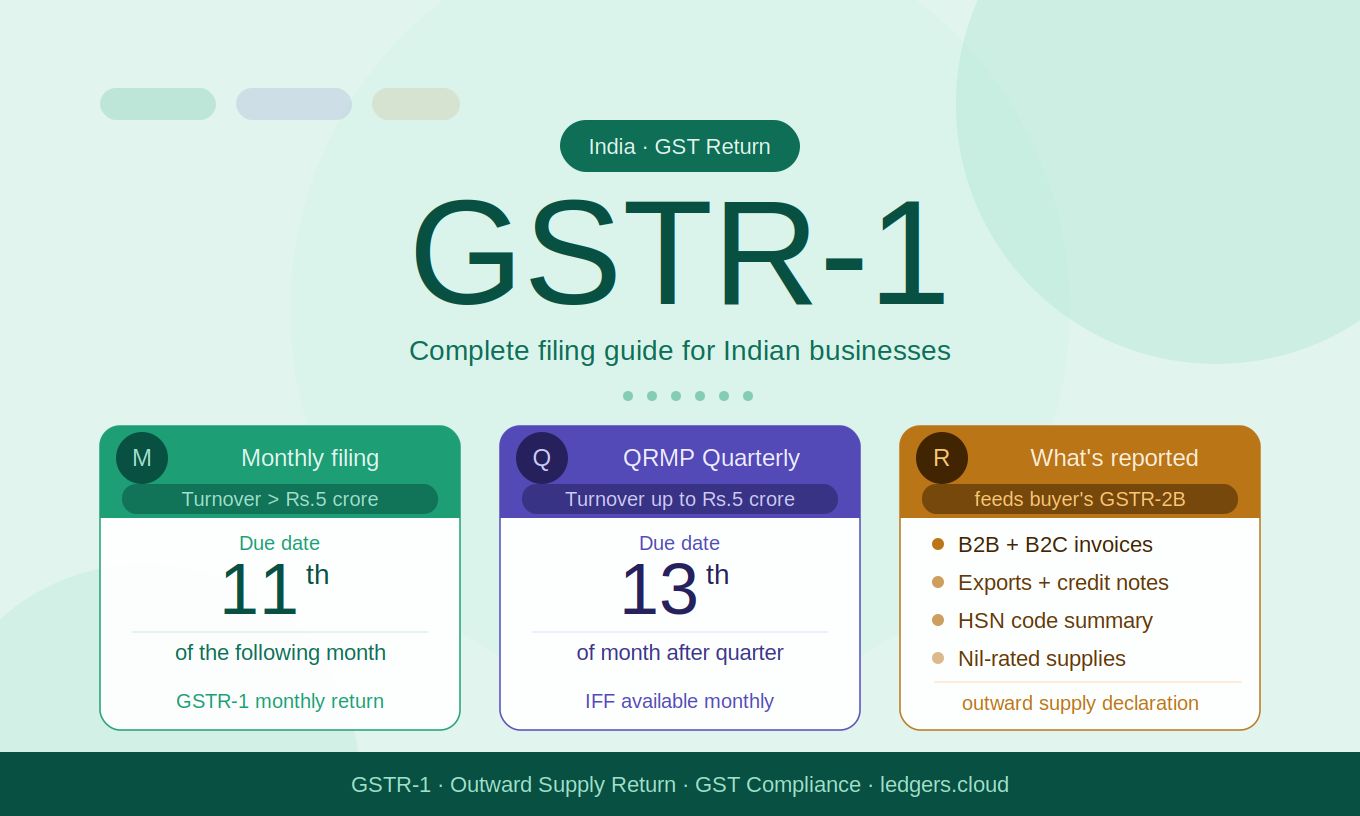

GSTR-1 is a monthly or quarterly GST return that captures every outward supply your business makes during a given period. In other words, it is a detailed record of all the sales invoices you have raised, the credit notes you have issued, and any amendments you need to make to earlier filings.

Every GST-registered supplier who makes taxable outward supplies is required to file GSTR-1. This includes regular taxpayers, SEZ units, and casual taxable persons. Composition scheme dealers and Input Service Distributors are among the few who are exempt from filing it.

The data you report in GSTR-1 is not just for compliance. It directly feeds into your buyer's GSTR-2B, which is their auto-generated input tax credit statement. So when you file accurately and on time, you are not just ticking a regulatory box. You are actively helping your customers claim the ITC they are entitled to. That matters for business relationships.

Who Needs to File GSTR-1 and How Often?

The filing frequency depends on your annual aggregate turnover:

Monthly filing applies to businesses with a turnover exceeding Rs. 5 crore in the previous financial year. The due date is the 11th of the following month.

Quarterly filing under the QRMP (Quarterly Return Monthly Payment) scheme applies to businesses with turnover up to Rs. 5 crore. The due date falls on the 13th of the month following the end of the quarter.

If you are under the QRMP scheme, you can use the Invoice Furnishing Facility (IFF) to upload B2B invoices in the first two months of a quarter without filing a full return. This keeps your buyers' ITC flowing without waiting for the quarter to close.

What Goes Inside GSTR-1?

GSTR-1 covers a wide range of supply types, each reported in a separate table. Here is a practical breakdown of what you will be filling in:

B2B Invoices (Table 4): All taxable invoices issued to registered businesses. Since your buyers will use this data for ITC, accuracy here is critical.

B2C Large (Table 5): Invoices raised to unregistered customers where the invoice value exceeds Rs. 2.5 lakh for interstate supplies.

B2C Small (Table 7): All remaining B2C invoices, reported as consolidated state-wise figures rather than individual invoice entries.

Credit and Debit Notes (Tables 9 and 9B): Any adjustments made to previously issued invoices, whether due to returns, price changes, or errors.

Exports (Table 6): Supplies made outside India, whether with or without payment of IGST.

Nil-Rated, Exempt, and Non-GST Supplies (Table 8): These need to be declared even though no tax is collected on them.

HSN Summary (Table 12): A summary of supplies based on HSN (Harmonized System of Nomenclature) codes, giving the government a product-level view of what you have sold.

Common Mistakes That Can Cost You

A few errors tend to trip people up repeatedly:

Mismatched invoice numbers between your books and GSTR-1 create reconciliation headaches for both you and your buyers. Make sure your invoicing software maintains consistent numbering.

Missing credit notes is another common gap. If you issued a credit note during the period, it must be reported in GSTR-1. Skipping it means your buyer's GSTR-2B will show a higher ITC than they are actually entitled to.

Incorrect GSTIN of the buyer means the invoice will not reflect in the right taxpayer's portal data. Always verify GSTINs before raising invoices.

Late filing attracts a late fee of Rs. 50 per day (Rs. 20 per day for nil returns), capped at Rs. 10,000. It also blocks you from filing GSTR-3B for the same period in some cases, which compounds the problem.

The Link Between GSTR-1 and Your Invoices

Everything in GSTR-1 starts with your invoice. A well-structured GST invoice with the right GSTIN, HSN code, tax breakup, and place of supply makes GSTR-1 filing almost automatic. When your invoicing process is clean, your return filing is clean.

This is exactly why having a reliable invoicing tool matters as much as any other part of your compliance workflow. Generating accurate GST invoices from the start eliminates the need to manually reconcile mismatches later. Ledgers makes this straightforward by letting you create GST-compliant invoices in seconds, with all the fields pre-structured to match what GSTR-1 expects.

A Few Tips to Make GSTR-1 Filing Easier

Reconcile before you file. Cross-check your sales register against the invoices uploaded on the GST portal. Catching discrepancies before submission is always easier than amending after.

Use auto-population. The GST portal auto-populates certain data from e-invoices and e-way bills. If you are using e-invoicing, a significant portion of your GSTR-1 data will already be filled in. Review it rather than re-enter it.

Do not wait for the deadline. Filing a few days early gives you time to fix errors without the pressure of a looming due date. It also ensures your buyers see your invoice data sooner, which helps them with ITC planning.

Wrapping Up

GSTR-1 is one of those compliance requirements that feels heavier than it actually is once you have a system in place. The core idea is simple: report what you sold, to whom, and how much tax was collected. The complexity comes from the volume of transactions and the need for precision at every step.

Getting your invoicing right is the single best thing you can do to make GSTR-1 manageable. When every invoice is accurate and properly structured, your return practically fills itself.