PUGALENTHI

Senior Developer

Updated on

16-04-2026

Impact of Blocked Credits Under GST (Section 17(5))

Navigating India's Goods and Services Tax (GST) represents a major challenge to entrepreneurs attempting to maximize their financial working capital efficiency. An important provision of GST is the ability for the Input Tax Credit (ITC) to be claimed against the total liability of GST paid for all goods and/or services purchased. However, there are limitations to claiming ITCs through the concept of blocked credits, which are detailed through Section 17(5) of the GST Act. These blocked credits limit a company's eligibility to claim ITCs resulting from the purchased item or service. As a result, companies who are limited by blocked credits will typically experience diminished financial and operational efficiencies. This article reviews and provides insight into the blocked credits concept, its effect upon companies, typical mistakes leading to blocked credits as well as recommended practices to ensure compliance with GST legislation.

Understanding Input Tax Credit (ITC) and Its Importance

ITC serves as a fundamental aspect of GST, designed to alleviate the cascading tax burden and promote a seamless flow of goods and services without the hindrance of cumulative tax liabilities. In essence, ITC allows businesses to claim the tax paid on procurements (input GST) against their output GST liabilities, thereby minimizing the overall tax outflow. This not only aids in reducing the cost of goods and services but also bolsters a business's cash flow management, enabling resources to be directed towards growth and expansion.

What Are Blocked Credits Under GST Section 17(5)?

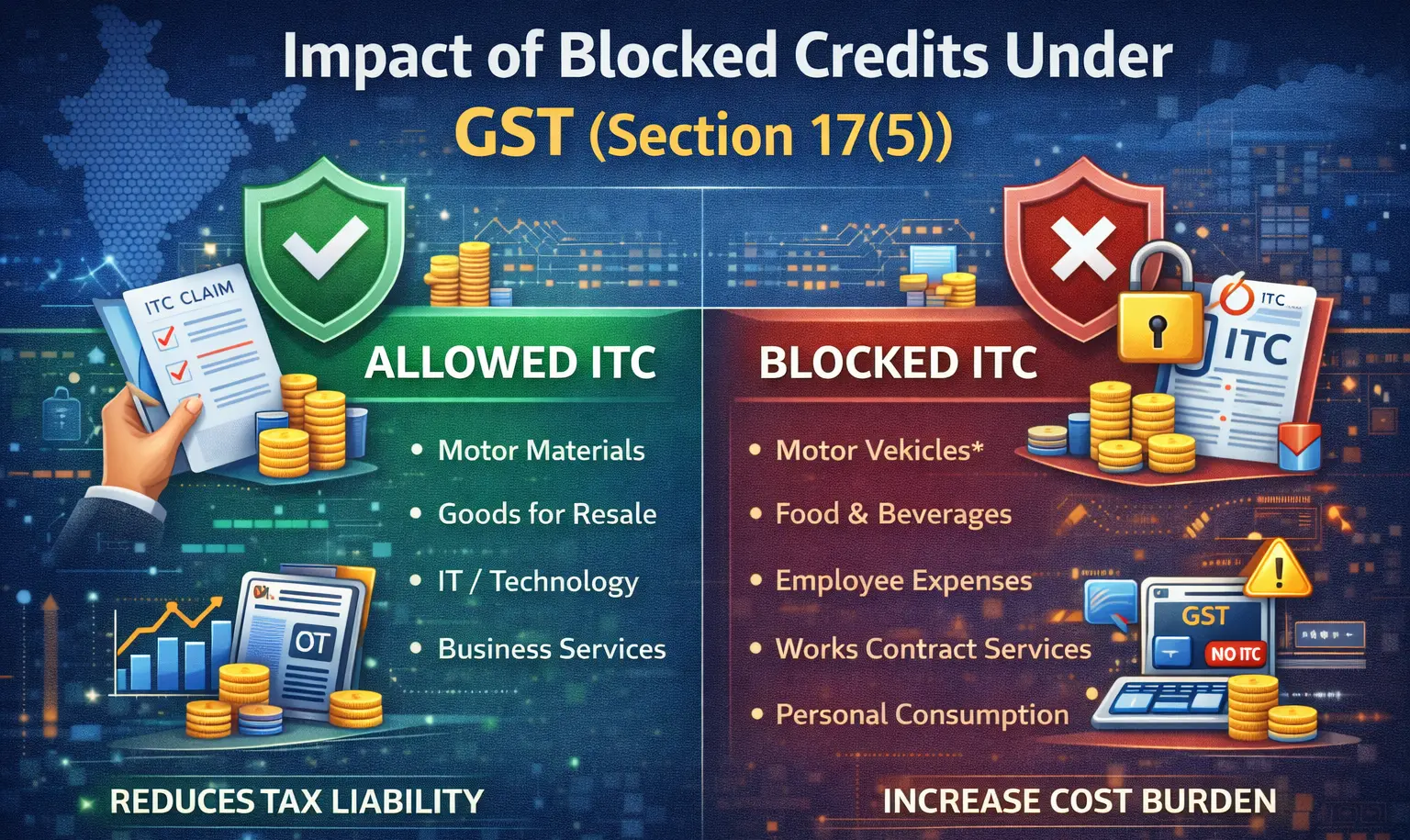

While ITC is a valuable mechanism to counterbalance tax burdens, not all expenses qualify for credit under GST. Section 17(5) explicitly categorizes 'blocked credits,' disallowing ITC on specific items, regardless of a business's sector or operational nature. Compliance with these provisions is crucial to avoid legal repercussions, maintain accuracy in financial reporting, and ensure effective tax management.

Key Categories of Blocked Credits

- Motor Vehicles: ITC is generally blocked for motor vehicles unless used for specific purposes such as transportation of goods or passengers. Exceptions include vehicles used for providing training on driving, flying, or navigating.

- Food and Beverages: Expenses incurred on food and beverages are typically ineligible for ITC. However, if these are part of a taxable outward supply of the same category, businesses may claim ITC.

- Employee-Related Expenses: Benefits provided to employees, including membership of clubs, health insurance, and travel, are largely not eligible for ITC. An exception applies if such obligations are mandated by law or provided as part of a contract for supply of service.

- Works Contract Services: ITC is disallowed for works contract services when supplied for the construction of immovable property except when such inputs are a composite supply of construction services.

- Personal Consumption: Any goods or services consumed personally by employees or business owners fall under blocked credits to prevent misuse of ITC provisions.

Financial and Compliance Impact of Blocked Credits

The financial implications of blocked credits are significant; they directly increase the operational costs of businesses, as they must bear the GST expense without offset benefits. The additional tax liability can strain cash flows, particularly for small and medium enterprises with limited resources. From a compliance perspective, accurately identifying and classifying expenses that fall under blocked credits is imperative to avoid penalties and maintain accurate tax returns.

Common Mistakes and How to Avoid Them

Among the common mistakes, businesses often inaccurately claim ITC on expenses that are classified as blocked credits due to ignorance or misinterpretation of the law. To mitigate such errors:

- Maintain clear and thorough documentation of purchases to support ITC claims.

- Regularly review GST guidelines and updates to stay aligned with the latest compliance requirements.

- Employ robust GST software or consult with tax experts to enhance accuracy and efficiency in ITC management.

Best Practices for ITC Compliance

Ensuring compliance with GST laws regarding blocked credits necessitates vigilance and strategic planning:

- Classification: Maintain comprehensive records categorizing all purchases and expenses to distinguish between eligible and ineligible ITC.

- Documentation: Preserve invoices and receipts meticulously to support the legitimacy of ITC claims and facilitate smooth audits.

- ITC Reconciliation: Regularly reconcile ITC statements with GST returns to identify discrepancies and rectify them promptly.

- Expert Consultation: Seek guidance from GST consultants or leverage specialized software solutions for streamlined ITC management.

Conclusion

Blocked credits under Section 17(5) of GST create both financial and compliance difficulties for businesses throughout India. The ability to effectively manage your ITC needs to be based upon a thorough understanding of blocked credits as they relate to GST regulation; therefore, your knowledge of these regulations is critical to your understanding of the complexities associated with the overall process. Companies can take advantage of expert input and implement best practices to maximize their ITC claims, which will have a positive impact on their cash flow and operational efficiency. Enriching your knowledge and adjusting to continuously changing GST regulations are also key points; therefore, it is paramount for you to seek professional assistance when it comes to developing effective tax management strategies.

LEDGERS

LEDGERS assists with compliance relating to GST through the integration of reconciliations into your accounting processes to allow the speedy identification of errors in records prior to incurring any penalties or interest. LEDGERS allows you to automate the process of synchronizing your GSTN data and tracking invoices on an invoice-by-invoice basis eliminating the need for manual corrections and the time-consuming process of verifying transactions at the end of a reporting period through the use of automatic validations from the system to facilitate revenue compliance activities.