PUGALENTHI

Senior Developer

Updated on

07-04-2026

Turnover Limits Under GST: Updated Rules Explained

With fast changing economy of India, understanding the Goods and Services Tax (GST) has become essential for companies. A key component to properly comply with GST laws is to understand what the Turnover Limits Are Under GST since this information assists in determining if you require to register. This article explains the current turnover limit thresholds under GST and discusses how these impact businesses throughout the country.

Understanding Aggregate Turnover and Its Importance

An individual's Aggregate Turnover refers to the total value of all taxable/exempt supplies made by the individual (including exports) within one financial year including any inter-state supplies made within the same financial year under one PAN. However, deductions are made for any inward supplies made under the Reverse Charge Mechanism, GST and CESS paid to the Governments through the Individual's registered office. This means that the GST registrant can determine if he/she exceeds the Aggregate Turnover threshold which defines whether or not he/she must register under the GST.

Why Are Turnover Limits Important?

Turnover limits serve as thresholds for mandatory GST registration. They ensure that all business entities meeting a specific turnover requirement comply with GST regulations. Understanding and maintaining accurate records of turnover helps businesses avoid penalties and ensures smooth operations.

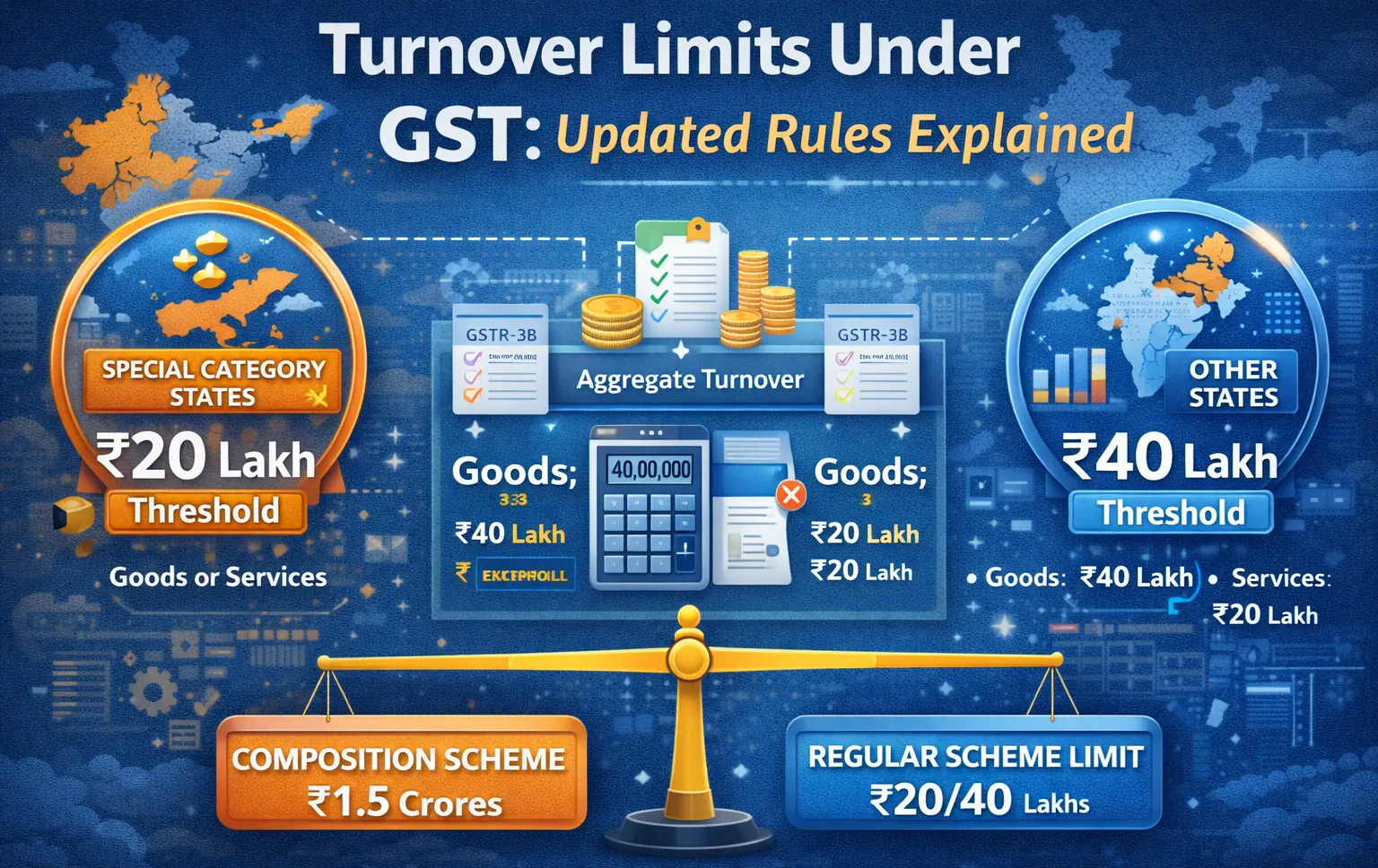

Current GST Registration Thresholds

Let's explore the current threshold limits for GST registration, which differ based on the type of goods, services, and the location of the business:

- For goods: Businesses with an aggregate turnover exceeding INR 40 lakhs are required to register for GST.

- For services: The threshold is set at INR 20 lakhs, reducing to INR 10 lakhs for special category states.

Special Category States

Special category states such as Arunachal Pradesh, Assam, Jammu and Kashmir, and others have a lower registration threshold due to their unique economic conditions. Businesses in these states need to be particularly attentive to these limits to maintain compliance.

Mandatory vs. Voluntary Registration

While many businesses are required to register for GST once they exceed the turnover threshold, some opt in voluntarily to take advantage of input tax credit and improve their market competitiveness. However, registration comes with the responsibility of GST compliance, which some smaller entities might find burdensome.

The Composition Scheme: Turnover Limits and Benefits

The Composition Scheme allows eligible businesses to pay taxes at a lower rate with fewer compliance burdens. Businesses with an aggregate turnover not exceeding INR 1.5 crores can opt for this scheme.

- The scheme simplifies tax calculation and reduces compliance requirements.

- Businesses under the Composition Scheme cannot collect GST from customers.

Yet, the scheme is not available for interstate suppliers or certain service providers, demanding careful consideration before opting in.

How to Calculate Your Turnover

Accurate calculation of turnover involves considering all taxable and exempt supplies, interstate trading, and exports. Here’s how businesses can approach it:

- Include all sales and supply figures before adding GST.

- Account for exempt supplies, as they contribute towards aggregate turnover.

- Incorporate all interstate supplies and exports.

Practical Example: If a Delhi-based business supplies INR 30 lakhs exempt supplies, INR 60 lakhs taxable supplies, and has INR 15 lakhs in exports, their aggregate turnover is INR 105 lakhs, requiring GST registration.

Recent Updates and Changes

Recent GST rule changes have raised turnover limits for certain service providers and revised compliance requirements for startups and small businesses. Staying informed of these updates can save businesses from unnecessary penalties and enforcement actions.

Common Misconceptions in Turnover Calculation

One prevalent mistake is excluding exempt supplies from turnover calculations, leading to incorrect interpretations of GST liability. Additionally, many businesses misunderstand interstate supplies' impact on their turnover calculations.

Checklists and Best Practices for Ensuring Compliance

Businesses can enhance their GST compliance by creating a comprehensive checklist:

- Regularly update sales data in accounting software.

- Reconcile figures monthly to avoid discrepancies.

- Use GST software that automatically calculates turnover and GST liability.

Adopting these practices aids businesses in maintaining precise records and ensures seamless compliance with GST regulations.

Conclusion

Understanding and managing turnover limits under GST is essential for business compliance in India. As turnover thresholds and regulations continue to evolve, businesses must stay informed and vigilant to navigate these changes effectively. By embracing the right tools and practices, businesses can ensure adherence to GST rules, paving the way for sustainable growth and market competitiveness.

In this article, we have dissected the complex subject of GST turnover limits, offering clarity and practical guides for businesses. By taking informed actions, businesses can confidently navigate the GST landscape, minimizing risks and maximizing opportunities.

LEDGERS

LEDGERS assists with compliance relating to GST through the integration of reconciliations into your accounting processes to allow the speedy identification of errors in records prior to incurring any penalties or interest. LEDGERS allows you to automate the process of synchronizing your GSTN data and tracking invoices on an invoice-by-invoice basis eliminating the need for manual corrections and the time-consuming process of verifying transactions at the end of a reporting period through the use of automatic validations from the system to facilitate revenue compliance activities.